If you decide not to fight the foreclosure of your home, you don’t have to leave right away. Learn more.

If you don’t fight your foreclosure or take any steps to work out an alternative, the foreclosure will move forward on a schedule dictated by your lender’s and loan servicer’s workload and policies, and federal and state law.

You Don’t Have to Leave Right Away

The single most important point to understand is that you don’t have to leave your house just because you’re behind in payments or because foreclosure proceedings have started. In most states, you’ll probably be able to stay long enough to plan for the future by saving all or some of the money that you’re no longer putting toward the mortgage.

Example. Joshua and Ellen got in over their heads and now can’t afford the $3,000 monthly payment on their mortgage. They decide to let the house go. They already know that federal mortgage servicing law requires the servicer to wait at least 120 days after they quit making payments before officially starting the foreclosure. They then consult with a local foreclosure attorney to see how much more time they have. They learn that:

In their state, they’ll get notice about the foreclosure sale four weeks before it happens in what’s called a notice of sale.

They can file for Chapter 7 bankruptcy and delay the sale by three additional months. Bankruptcy will also let them leave without owing the lender anything. They otherwise could face a deficiency judgment in their situation.

Under their state’s laws, they’ll get to stay in the house during the redemption period after the foreclosure sale.

Altogether, they will have about a year of living in the house without making payments, and if they can save at least $2,000 a month, they will have roughly $24,000 in the bank when they set out to seek new shelter.

How Long You’ll Get to Stay In the Home

How much time you’ll get to remain in your house depends on many factors, including:

whether the foreclosure is judicial or nonjudicial (judicial foreclosures usually take longer than nonjudicial ones)

whether you get the right to participate in foreclosure mediation, which might prolong the process

whether you get the right to live in the home during a post-sale redemption period, if there is one, after the foreclosure sale, and

whether part of your strategy involves filing for bankruptcy before the foreclosure sale, which provides an additional two to three months’ delay.

Getting Help

To find out approximately how long you can remain in your home in a foreclosure in your state and in your situation, consider talking to a foreclosure attorney or a HUD-approved housing counselor.

Learn what you can do after the foreclosure sale, from staying in the home for a certain period of time to buying the property back.

If your home was recently sold in a foreclosure sale, but you haven’t yet moved out (or if you’re currently going through a foreclosure), you might want to know what happens next. Some homeowners quickly leave the home after the home is sold. However, depending on your circumstances and your state’s laws, you might have other options to either stay in the home for a longer period of time, get money to move out sooner, or even buy back the home.

Redeeming the Home

Some states permit a foreclosed homeowner to buy back the home within a certain period of time after the sale. This is called a redemption period. To redeem the home, you usually have to pay the total purchase price, plus interest, and any allowable costs, to the purchaser who bought it at the foreclosure sale. In some states, though, you’ll have to pay the total amount owed on the mortgage loan, plus interest and expenses.

The deadline and procedures for exercising a right of redemption varies from state to state, and not all states provide a redemption period after the sale.

Getting Help to Buy Back the Home

In order to redeem, the former homeowner has to come up with another source of financing. But getting a bank to lend you money after a foreclosure can be very difficult, even if you have a steady income, because your credit score will have taken a bit hit. (Learn how a foreclosure affects your credit score.)

Some special programs are available to help homeowners in this type of situation. For example, a program called Stabilizing Urban Neighborhoods (SUN) offered by a nonprofit organization helps foreclosed homeowners in Massachusetts, Maryland, Rhode Island, New Jersey, Illinois, Connecticut, and Pennsylvania by purchasing foreclosed properties and then reselling those properties back to the former homeowners, usually at current fair market value, with a new, fixed-rate 30-year mortgage. (Learn more about the SUN Initiative.)

Live in the Home During the Redemption Period for Free

If your state provides a redemption period after the sale, you sometimes have the right to live in the home payment-free during this time. For example, in Michigan, most homeowners get a six-month redemption period (some people get a year) during which time they can live in the home. (Under some circumstances, though, like if the foreclosed homeowner unreasonably refuses to allow the purchaser to inspect the home, the purchaser can begin an eviction sooner. )

By staying in the home during the redemption period, you can save money by living rent-free. This way you can use the money that you otherwise would have spent on housing to pay other bills and start rebuilding your credit. (To learn more about your rights during the redemption period in your state, if there is one, consider talking to a local foreclosure attorney.)

Remaining in the Home as a Tenant

In some cases, you might be able to remain in the home as a tenant after the foreclosure sale. For example, Freddie Mac offers a program that allows recently foreclosed homeowners to rent their home on a month-to-month basis, if Freddie Mac acquires the property as a result of foreclosure. (You can learn more about this program, called the Freddie Mac REO Rental Initiative, at the Freddie Mac website. If you want to find out if Freddie Mac owns your loan, go to www.freddiemac.com/mymortgage or call 800-Freddie.)

Live in the Home Until You’re Evicted

If you don’t move out after the purchaser gets title to the home (typically either after the sale or after the redemption period), the new owner (often the foreclosing party) will start eviction proceedings to remove you from the property. The length and procedures for the eviction process varies from state to state. In some cases, the foreclosing party can include the eviction as part of the foreclosure action—depending on your state’s law and the circumstances of your case—while in other instances, it will have to file a separate eviction action with the court.

You might receive a notice prior to the start of the eviction (called a Notice to Quit), which gives you a certain amount of time—for example, three days—to leave the home before the eviction officially starts. While you can stay in the home until you’re forcibly removed through the eviction process, it is generally best to leave the property before this time period expires.

Getting a Cash for Keys Deal

To avoid having to complete an eviction, the purchaser might offer you a “cash for keys” deal. With this arrangement, you agree to leave the home by a certain date, and in good condition. In exchange, the purchaser gives you a specified amount of cash to help pay for your relocation costs.

You can request a cash-for-keys agreement if the purchaser doesn’t offer you one. You can contact Result Capital for that.

Your credit score will take a hit after foreclosure, short sale, or deed in lieu of foreclosure. Learn more.

If you stop making payments on your mortgage loan, you’ll probably go through a foreclosure, which will damage your credit score. Even if you manage to avoid going through a foreclosure with a short sale or a deed in lieu of foreclosure, your credit score will take a major hit.

Read on to learn the basics about why credit scores matter, how they work, and how a foreclosure, short sale, or deed in lieu of foreclosure typically hurts your credit score.

Credit Scores: Why They Matter, How They Work

If you apply for home loan or other form of credit, like a credit card or a car loan, the creditor will take a look at your credit score from one or more of three major credit reporting agencies—Equifax, Experian, and TransUnion—as part of the process of figuring out whether or not to extend you the credit. Credit scores, in theory, indicate whether you’re likely to default on the loan. Generally, people with lower credit scores are more likely to default on payments than people with higher scores.

Your credit score is based on what’s in your credit report, including:

the payment history on your outstanding debts

how many debts you have and how much you owe

how long your credit history is

the different kinds of credit you have

whether you’ve recently applied for new credit, and

whether you’ve been through a foreclosure or have declared bankruptcy.

Credit scoring companies use “models” that analyze this data and then assign a credit score based on that information. Different companies use different scoring models so a person’s credit score usually varies by a few or many points depending on which company and model generated the score.

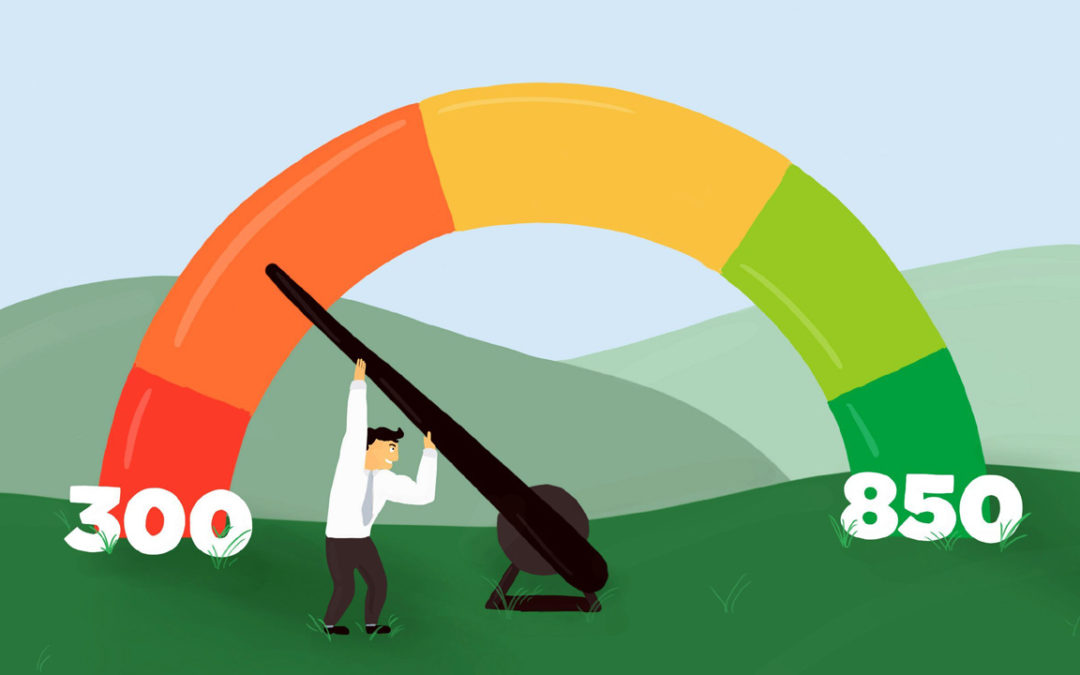

Typically, credit scores—like scores from the largest and most universal credit scoring company called FICO—range from 300 to 850. VantageScore, which is another credit scoring company, also uses a range of 300 to 850 in its newer model, while its older models have a range of 501 to 990.

How Foreclosure Affects Your Credit Score

Both missed mortgage payments and a foreclosure itself will damage your credit score.

How missed (or late) payments affect your score. Under federal mortgage servicing rules, in most cases, a borrower has to be more than 120 days delinquent on payments before the servicer can officially start a foreclosure. The lender reports the missed payments as 30 days late, 60 days late, 90 days late, and the like to the credit reporting agencies. According to FICO, a person’s credit score drops about 50 to 100 points when the lender reports the account as 30 days past due and each subsequent delinquency lowers the score further.

How foreclosure affects your score. After a foreclosure, your score will likely go down by at least 100 points. How much the score actually falls depends to some extend on your score before the foreclosure started. Someone with a higher score prior to a foreclosure generally loses more points than someone who already has a low score. According to FICO, a person who has a credit score of 680 prior to a foreclosure loses 85 to 105 points following a foreclosure. But a person who has a credit score of 780 prior to a foreclosure loses 140 to 160 points.

How a Short Sale or Deed in Lieu of Foreclosure Affects Your Credit Score

Completing an alternative to foreclosure, like a short sale or deed in lieu of foreclosure (DIL), will also usually hurt your credit score.

Generally, short sales and DILs have a similar effect on a person’s credit score. Much like with a foreclosure, if you have high credit score before the short sale or DIL—say you complete one of these transactions before missing a mortgage payment—the transaction will cause more damage to your credit score. Though, if you’re behind on your payments and already have a low score, a short sale or DIL won’t cause you to lose as many points as someone who has a high score.

Also, if you’re able to avoid owing a deficiency after the short sale or deed in lieu of foreclosure, your credit score might not fall quite as much.

Beware of Credit Repair Scams

Scammer credit repair companies sometimes try to sell their services claiming that they can easily repair your credit score or even clear a foreclosure off your credit report. However, foreclosures and many other negative items typically stay on a credit report for seven years and you can’t magically eliminate them—though the impact of these events on your score will lessen over time. Also, paying your other debts on time and disputing incomplete and inaccurate information in your credit report can improve your score.

Getting Help

If you want more information about how to improve your credit score, consider talking to a credit repair attorney. If you have questions about ways to avoid a foreclosure, consider talking to a foreclosure attorney or a HUD-approved housing counselor.

Federal laws protect homeowners when facing foreclosure.

On January 10, 2014, new federal laws that protect homeowners in the foreclosure process went into effect. These laws protect consumers by:

ensuring servicers provide assistance if a borrower is having difficulty making mortgage payments, and

protecting borrowers from wrongful actions by servicers.

Keep reading to learn more about these federal laws and how they might help you if you’re facing a foreclosure.

Why the Need for Laws Protecting Homeowners?

During the foreclosure crisis that began around 2008, the number of homeowners in financial distress increased exponentially and servicers simply couldn’t keep up with the increased demands for information and assistance. As a result, servicing errors were common and egregious.

Servicers Now Must Provide Homeowners With Assistance

Now, under federal law, servicers are supposed to work with borrowers who are having trouble making monthly payments.

Early Intervention Requirements: Servicer Must Contact the Borrower By Phone (or In Person) and In Writing

If a borrower falls behind in payments, a servicer must attempt to contact the borrower to discuss the situation no later than 36 days after the delinquency, and again within 36 days after each subsequent delinquency, even if the servicer previously contacted the borrower. If appropriate, the servicer must tell the borrower about loss mitigation options—like a modification, short sale, or deed in lieu of foreclosure—that might be available to the borrower. But, if you filed for bankruptcy or asked the servicer to stop communicating with you under to the Fair Debt Collection Practices Act (FDCPA), and the servicer is subject to this law, the servicer doesn’t have to try to contact you by phone or in person.

No later than 45 days after missing a payment, the servicer must inform the borrower in writing about loss mitigation options that might be available, and must do so again no later than 45 days after each payment due date so long as the borrower remains delinquent. The servicer does not, however, have to provide the written notice more than once during any 180-day period. If you’ve filed bankruptcy or asked the servicer not to communicate with you, it generally has to send a modified letter, subject to some exceptions.

Continuity of Contact Requirements: Servicer Must Appoint Personnel to Help the Borrower

The servicer must assign personnel to help the borrower by the time the borrower falls 45 days delinquent. The personnel should be accessible to the borrower by phone and able to respond to borrower inquiries.

When applicable, the servicer’s personnel should help the borrower pursue loss mitigation options, like by advising the borrower about:

available loss mitigation programs

how to submit a complete loss mitigation application

the status of a submitted application

how to appeal (if the application is denied), and

the circumstances when the servicer may refer a file to foreclosure.

The servicer may assign a single person or a team to assist a delinquent borrower.

Restrictions on Dual Tracking

Federal law also restricts “dual tracking.” Dual tracking happens when a servicer simultaneously evaluates a borrower for a loan modification (or other loss mitigation option) while at the same time pursuing a foreclosure.

Restrictions on Starting Foreclosure

Servicers generally can’t start a foreclosure until the loan obligation is more than 120 days delinquent, which provides time for the borrower to submit a loss mitigation application. A borrower is considered delinquent starting on the date a periodic payment sufficient to cover principal, interest, and, applicable, escrow becomes due and unpaid, until such time as no periodic payment is due and unpaid.

What is the first foreclosure notice or filing? In a judicial foreclosure, this means the foreclosing party can’t file a lawsuit in court to start the foreclosure until you’re more than 120 days behind. If the foreclosure is nonjudicial, the foreclosing party can’t begin the foreclosure by recording or publishing the first notice until you’re more than 120 days late in payments. If your state’s foreclosure laws don’t require a court filing or any document to be recorded or published as part of the foreclosure process, the first notice is the earliest document that establishes, sets, or schedules a date for a foreclosure sale.

Further restrictions on starting a foreclosure. Even if a borrower is than 120 days delinquent, if that borrower submits a complete loss mitigation application before the servicer makes the first notice or filing required to initiate a foreclosure process, the servicer can’t start the foreclosure process unless:

the servicer informs the borrower that the borrower is not eligible for any loss mitigation option (and any appeal has been exhausted)

the borrower rejects all loss mitigation offers, or

the borrower fails to comply with the terms of a loss mitigation option such as a trial modification.

To learn more about how foreclosure works in your state, see our Key Aspects of State Foreclosure Law: 50-State Chart.

Restrictions on Continuing Foreclosure After the Borrower Requests Help

If the servicer has already started a foreclosure and receives a borrower’s complete loss mitigation application more than 37 days before a foreclosure sale, the servicer may not move for a foreclosure judgment or order of sale, or conduct a foreclosure sale, until one of the three conditions mentioned above has been satisfied.

A Motion to Reschedule the Foreclosure Sale Doesn’t Violate Federal Law

While federal law generally prohibits a servicer from moving for a foreclosure judgment or an order of sale after a borrower submits a complete loss mitigation application, the U.S. Court of Appeals for the 11th Circuit held that a motion to reschedule a previously set foreclosure sale doesn’t violate this law. (See Landau v. RoundPoint Mortgage Servicing Corporation, 925 F.3d 1365, 27 Fla. L. Weekly Fed. C 2045, (11th Cir. June 11, 2019)).

The servicer doesn’t have to review multiple applications after you become delinquent on the loan. But if you bring the loan current after submitting an application, you may submit another.

Applicability of the Laws

These laws apply to mortgage loans that are secured by a property that is the borrower’s principal residence. The determination of principal residence status depends on the specific facts and circumstances regarding the property and applicable state law.

For example, a vacant property might still be a borrower’s principal residence under certain circumstances, like when a servicemember relocates due to permanent change of station orders and was living at the property as his or her principal residence immediately prior to displacement, intends to return to the property at some time in the future, and doesn’t own any other residential property.

Getting Help

If you’re having trouble making your mortgage payments, consider submitting a loss mitigation application to your loan servicer. Once submitted, under federal law, the servicer has five days to tell you whether it needs more information—so long as you submit the application 45 days or more before a foreclosure sale—and, if so, what information it needs.

Generally, the servicer is required to evaluate the application for all loss mitigation options within 30 days, as long as you submit the complete application more than 37 days before a foreclosure sale. Also, you may generally appeal a loan modification denial so long as the servicer received the complete loss mitigation application 90 or more days prior to a scheduled foreclosure sale. Remember, the servicer is required to review you for a loss mitigation option only once, unless you bring the loan current after submitting your complete application.

If you have questions about the foreclosure process in your state or about the laws discussed in this article, consider talking to a foreclosure attorney. If you want to learn about different loss mitigation options or you need help with your loss mitigation application, consider contacting a HUD-approved housing counselor.

If you’re facing a foreclosure, be on the lookout for foreclosure rescue companies—specifically, mortgage modification companies—that falsely claim they can help you save your home.

If you’re a homeowner struggling to make your mortgage payments and facing a possible foreclosure, a scammer might try to contact you. Scammer people and companies say that they help homeowners save their home—usually through a mortgage modification—but often leave homeowners in worse shape than before.

Mortgage Modification Scams

Borrowers who’re struggling to make their mortgage payments might have a number of options to get caught up on the payments, including a modification, forbearance agreement, or repayment plan. You can apply for any of these options, including a modification, on your own without paying for assistance. But scammers might send you mailings trying to convince you that you’re better off hiring their company to help you with the process. (To learn what to do—and what not do—in the modification process, read Do’s and Don’ts for Getting a Loan Modification.)

Solicitations and mailings that you get from a modification company tend to look official, even though they aren’t. The name of the company might sound like the government has endorsed the program or the mailing might refer to official U.S. government programs. Typically, scammer mailings claim you can “Stop foreclosure now!” or “Over 90% of our customers get a loan modification.” These statements are ploys to get you to call the company. Once you do, the main goal of a scammer modification company is to separate you from your money by getting you to pay for the company to—supposedly—help you get a modification.

Forensic Loan Audits and Securitization Audits

A modification company might try to convince you to pay for a “forensic loan audit” or a “securitization audit” to improve your chances of getting a mortgage modification.

What’s a Forensic Loan Audit?

In a forensic loan audit, in theory, a loan auditor reviews paperwork from when you took out your mortgage to see if the lender complied with the law. If the audit reveals legal violations, you can supposedly then use the results to strong-arm the lender into giving you a modification. But the way most companies conduct the audit is that a processor enters your information into a compliance software program, and the program prepares a very basic report. In most cases, no errors or only minor errors are found. The sales person might say that the results of such an audit will force the servicer into giving you a modification, but this is rarely true.

What’s a Securitization Audit?

In a process called securitization, multiple loans with similar characteristics are pooled and then sold in the secondary market, often to a trust. A securitization audit will supposedly reveal whether your loan was securitized and, if so, whether the securitization was done correctly. But securitization audit reports usually just give you publicly available information and make unsupported conclusions of law that aren’t useful when trying to get your loan modified.

Modification Companies: High Fees for Little or No Services

Most foreclosure scammers, including modification companies, exploit a homeowner’s trust and desperate situation by:

charging very high fees for services the homeowner could easily do without assistance, like sending in documentation to the servicer

charging money for certain services and then not doing anything to earn the fees, or

taking steps that actually hurt the homeowner, like missing deadlines or allowing a foreclosure sale to happen.

There’s nothing that a modification company can do that you can’t do yourself. In fact, the company might even hurt your chances of getting a modification, like if it:

neglects to send in your paperwork to the servicer (the company you make your payments to, which also handles modification applications)

sends the wrong documents to the servicer, or

fails to return the servicer’s phone calls.

By the time you realize the company is just running a scam, there might not be enough time to reinstate the loan, work out an alternative to foreclosure, sell the home, or find effective assistance. In almost all cases, you’re better off applying for a modification directly with the servicer yourself or—if you find the servicer is unhelpful or is dual tracking your application—hiring a reputable attorney to help you.

Some States Have Laws to Prevent Foreclosure Rescue Scams

To protect homeowners in financial difficulty from losing their homes to foreclosure rescue scams, the Florida legislature enacted the Foreclosure Rescue Fraud Prevention Act. This law imposes tight restrictions on anyone offering services purporting to help you save your residential property from foreclosure. New Jersey also has a law designed to prevent foreclosure consultants from taking advantage of distressed homeowners.

Tips to Help You Avoid Becoming the Victim of a Modification Scam

Here’s how you can make sure that you don’t become a victim of a modification scam.

Don’t pay upfront fees. If a modification company demands a large upfront fee from you, beware. Many states have laws prohibiting modification companies from collecting money before performing services, as well as other restrictions on foreclosure rescue activities.

Don’t pay a modification company rather than your servicer. Sometimes, modification companies advise people to pay the company’s fee instead of making their mortgage payments. This is a red flag. The company might take your money, fail to get you a modification (or not even try), and then you’ll be even further behind on your payments.

Don’t ignore your servicer or lender. Modification companies often tell people to stop communicating with their servicer and let the company do all negotiating. But that’s not a good idea. You should continue to talk (and listen) to your loan servicer. There’s no magic trick or secret skills involved in “negotiating” a modification. You submit an application and the servicer will let you know if you qualify. Plus, if you keep the lines of communication open, you might learn about a workout option you hadn’t previously considered.

Do work with a HUD-approved housing counselor. If you need help working out a modification, you can get free help from a HUD-approved housing counseling agency.

Reporting Scams

If you suspect you’re a victim of a modification scam, contact:

Learn about common mistakes and errors that happen in the mortgage servicing industry.

Mortgage servicers collect and process payments from homeowners, as well as handle loss mitigation applications and foreclosures for defaulted loans. Unfortunately, servicers sometimes make errors when it comes to managing homeowners’ accounts.

Common Errors in the Mortgage Servicing Industry

Servicers sometimes engage in harmful servicing practices that can cause a borrower to default on the loan or otherwise lead to foreclosure. Below are some common ones.

Misapplication of Payments or Inaccurate Accounting

One of the duties of a servicer is to collect and process payments from the borrower. But in some cases, a servicer might:

improperly apply funds (in violation of the terms in the mortgage or deed of trust)

ignore a grace period, or

fail to credit funds to the correct account.

Example. Let’s say a borrower sends in a proper monthly payment of $1,200, but the servicer incorrectly records the payment as $200 and places this amount in a suspense account. (Servicers often use suspense accounts when partial payments are received from a borrower.) The servicer then reports the payment as late to the credit reporting agencies. The servicer’s actions could affect the homeowner’s credit score, even if the mistake is eventually corrected.

The prompt crediting rule. Under federal mortgage servicing rules, the servicer must credit your payment to the account on the day it receives the payment. This is called the prompt crediting rule. But there are a few exceptions to this rule. The servicer doesn’t have to apply the funds to the account on the day the payment comes in if any of the following are true.

The servicer doesn’t charge you anything—like a late fee, additional interest, or any similar penalty—due to the delay.

The servicer doesn’t report negative information to a consumer reporting agency.

You didn’t follow the servicer’s written instructions on how to make your payment. Payments that don’t comply with the servicer’s specific instructions must be credited within five days of receipt.

You actually made a partial payment. (A partial payment occurs when you pay less than the full amount due, including principal, interest, and escrow, if applicable.)

Partial payments and suspense accounts. The servicer may place a partial payment into a suspense account rather than applying it to your account. If the servicer places your payment into a suspense account, it must let you know on your next monthly statement (called a “periodic statement”) that it has decided to hold the funds in suspense rather than applying them to your account. Once you make another payment and there are enough funds in the suspense account to cover a full payment—including principal, interest, and any applicable escrow amounts—the servicer must then apply the funds to the account.

Charging Unreasonable Fees

Loan contracts generally allow a servicer to charge fees under certain circumstances, like when the borrower is late on a payment or is in foreclosure. A few examples of these types of fees are:

late fees

inspection fees

foreclosure costs, and

other default-related fees.

But servicers sometimes charge excessive fees or incorrect amounts to the account, which unfairly increases the total balance owed by the borrower. (Learn more in Challenging Late & Other Fees in Foreclosure.)

Improperly Force-Placing Insurance

Most mortgages and deeds of trust require homeowners to maintain hazard insurance coverage on their property. The property owner will generally purchase a homeowners’ policy to meet this requirement. But if the homeowner lets the coverage lapse, the servicer can obtain insurance coverage at the homeowner’s expense. This is called “force-placed” or “lender-placed” insurance. Usually, the servicer adds the cost of the force-placed insurance to the loan payment.

Sometimes, a servicer force-places insurance coverage even though the borrower already had other coverage in place. Because force-placed insurance is expensive, these charges can increase the monthly payment by a large amount. As a result, a homeowner who is already behind in payments or is facing financial difficulties might go into foreclosure when it becomes even more difficult to keep up with the monthly payments.

Dual Tracking

Dual tracking occurs when the servicer proceeds with foreclosure while simultaneously working with the borrower on a loan modification. With dual tracking, the foreclosure might be completed even though the modification application is still pending.

Efforts have been made to address and correct this problem: Federal law restricts dual tracking and some states, like California and Colorado, have laws that prohibit dual tracking.

Failing to Make Appropriate Escrow Disbursements

Escrow accounts are established to ensure that real estate taxes and homeowners’ insurance get paid. Along with the monthly mortgage payment for principal and interest, the servicer collects funds from the borrower that will be used to make payments for these expenses on behalf of the borrower. But, in some cases, the servicer neglects to make the tax or insurance payment.

Consequently, a homeowner could face penalties from the taxing authority (and, in a worst-case scenario, a tax foreclosure) or face difficulties with uninsured property damage. Additionally, the servicer might charge a late fee imposed by the taxing authority or reinstatement fee imposed by the insurance company to the borrower’s account. These fees could possibly lead to an escrow shortage, which in turn would increase the borrower’s monthly payments.

KNOWLEDGEABLE FORECLOSURE PROCESS LAWYERS IN CALIFORNIA

Most California residents have heard of the concept of foreclosure and are no doubt aware of the prevalence of foreclosures during the 2008 housing crisis. But few understand how the mortgage foreclosure process actually works, or what banks and lenders must do to reclaim your home.

While many may believe that foreclosures are a judicial process that requires a lender to go before the courts in order to work out your financial issues, this is not usually the case. Most foreclosures in California are non-judicial and happen through a more administrative process.

FORECLOSURES IN RANCHO CUCAMONGA

The foreclosure process in California begins with the owner of the property, when he or she misses the first payment on a mortgage loan. This could be for any number of reasons – perhaps a family member loses their job, or an urgent medical crisis arises. Regardless of the circumstances, the failure to make a timely payment puts the bank on notice that the owner may have a problem.

Missing a payment by a few days usually is not a problem, as long as a homeowner quickly rectifies the issue and makes the payment as soon as possible. Rather, real issues begin to arise when the homeowner goes into default. Default typically occurs when the homeowner is behind on payments for 90 days.

A notice of default is the second step in the foreclosure process. This will happen after the homeowner enters default. The mortgage lender will typically file a notice of default with the court, and must then provide the owner with a copy within ten days. The owner’s copy will explain why the owner is in default and the options for getting out of default.

Depending on the bank or mortgage lender, an owner may be able to create a payment plan that will help to get out of default, and pay off all outstanding loan payments, interest, and fees.

When The Bank Or Lender Is Not Getting Paid

After an owner receives a notice of default, most lenders will give them three months to bring the loan current and make all outstanding payments. At the 180 day mark (90 days after default), the lender may begin official foreclosure on the home if the owner is still unable to pay.

Foreclosure means that the bank can attempt to auction off the home to recover the money that it has lended that the owner is no longer able to repay. This is usually done through what is known as a trustee sale. When the bank decides to go this route, it will notify the owner by providing a notice of trustee sale that sets the date for the auction of the home.

The bank must give the owner up to 20 days after the service of a notice of trustee sale to actually hold the auction to sell the home to the highest bidder. This may give the owner some last ditch opportunities to attempt to recover the home, either through negotiation or through the courts.

If the house does sell, the owner will be relieved of your financial obligations to the lender, even if the house sells for less than the amount that is currently owed on the loan. At the time of sale the owner loses both access to the home and responsibility for the debt incurred.

CALIFORNIA ATTORNEYS HELPING ALL PARTIES THROUGH THE FORECLOSURE PROCESS

The foreclosure process can be difficult for all parties involved, including lenders, banks, and the debtor who owns the mortgage. Having a clear understanding of the process involved can go a long way toward avoiding disputes or difficulties in the process. At CKB Vienna LLP our mortgage and banking attorneys have assisted clients on both side of the transaction through the foreclosure process and are equipped to handle simple foreclosures or complicated transactions. For more information, contact us online or at 909-980-1040.

Sometimes life takes us down a bumpy path, which can leave us in less than ideal situations like bankruptcy or foreclosure. That was the unfortunate case so many people found themselves in during the housing crisis nearly 10 years ago. But now, with more emphasis on licensing mortgage bankers, increasing ethical standards and laws, and a better job market, the future looks brighter. That’s not to say many people aren’t still impacted by the crash.

If you’re someone who went through bankruptcy and/or foreclosure during the housing crisis, you might think you can’t get another home loan. But before you settle for renting, consider this: It’s possible to qualify for a mortgage even after bankruptcy or foreclosure. The future really does look brighter now, doesn’t it?

HOW DO BANKRUPTCIES AND FORECLOSURES HAPPEN?

Often times, it’s longterm unemployment that can result in a foreclosure. Foreclosures are a result of not being able to pay your mortgage. Basically, if you miss a payment deadline, your lender can take your home to take care of the debt. During this process, lenders will notify credit bureaus, which will likely harm your credit. The thing is, lenders don’t like foreclosures. It’s actually quite expensive and time consuming for them. So if you think you might miss a payment, it’s better to be proactive and talk to your lender about possible options to avoid foreclosure.

A good way to stay aware of your payment due dates is to check your promissory note, which also includes information on when and how much late fees are.

If you’re unable to pay your mortgage, your lender will take your home to pay off debt through the legal action of foreclosure. They then sell the home, and then whatever is left over is what you’re still required to pay. For example, if you borrowed $250,000 and the foreclosed home sold for $100,000, then you still owe $150,000. This is called a “deficiency on the loan.”

The problem is, other than not having a home, if you don’t have a job, it’s a bit unrealistic to pay off the deficiency. After all, not having a job is what possibly got you here in the first place. So, this leads homeowners to the next step – bankruptcy. In this case, you may file for Chapter 7 bankruptcy, where you include your mortgage and house and liquidate those assets to rid yourself of any debt. Another option is Chapter 13 bankruptcy, which essentially allows you to repay your debt in installments.

Homeowners sometimes file for bankruptcy, often times after the foreclosure has occurred and they can’t pay off the deficiency. But people can file for bankruptcy for different reasons unrelated to homes, and it doesn’t always involve a foreclosure.

Filing for bankruptcy is not ideal, but sometimes its the only solution given certain circumstances, and it can ultimately help you get a fresh start and possibly receive a second chance.

The good news is, although many believe this is the end for them, in reality, it’s still possible to get another home down the road.

WAITING PERIODS FOR LOANS

There are a few different loans you could potentially choose from in the event of post-filing of bankruptcy. The ones that are a bit more forgiving are government-insured loans. Since your credit won’t be stellar, choosing between FHA, VA loan, or USDA could be your best bet, as long as you qualify for one of them.

If you don’t qualify for any government-insured loans, but do for a conventional loan, then the wait time is a bit different. Here are the generalwait times for loans:

FHA

Chapter 7 bankruptcy: 2 years

Chapter 13 bankruptcy: At least 1 year of satisfactory payments and court’s approval

Foreclosure: 3 years

VA loan

Chapter 7 bankruptcy: 2 years

Chapter 13 bankruptcy: At least 1 year of satisfactory payments and court’s approval

Foreclosure: 2 years

USDA

Chapter 7 bankruptcy: 3 years

Chapter 13 bankruptcy: At least 1 year of satisfactory payments and court’s approval

Foreclosure: 3 years

Conventional loan

Chapter 7 bankruptcy: 4 years

Chapter 13 bankruptcy: 2 years from discharge date or 4 years from dismissal date

Foreclosure: 7 years

Also keep in mind guidelines can vary depending on when your foreclosure and bankruptcy were filed and reasons behind the filings. There are some differences between the outcome of the bankruptcy in terms of “dismissal” vs. “discharge,” as well as foreclosure “completion date” vs. “disbursement date.” The completion date is the date the lender foreclosed, and the disbursement date is the date that the lender or bank sold the home to someone else.

REBUILD YOUR CREDIT AND PREPARE FOR THE MORTGAGE APPLICATION

While you wait things out before applying for a mortgage again, a good step forward in the right direction would be to work on rebuilding your credit.

As you are aware from your first purchase, credit scores play a big part in the loan you qualify for. Here are a few things to consider doing:

Check your credit report first to know where you stand.

Keep balances low and pay off any balances in a timely manner instead of moving it around.

Stay current on your payments. The longer you stay current, the more your score should increase with time.

Set up reminders to help you stay on top of your payments.

Don’t open up a bunch of credit accounts in a short-period of time, and don’t close unused credit cards, especially in a short period of time. Closing them won’t make them go away.

Introduce a good mix of different types of credit.

Consider applying for a credit-builder loan which basically helps you build your credit like a forced savings account. It makes you put money away each month that you’ll get in the end.

Talk to your mortgage banker for more unique tips that are better tailored to you.

It’s tough to go through bankruptcy and foreclosure, but you’re not alone, and we get it. So just keep in mind it’s possible to turn things around and improve your financial situation with some dedication, research, help from your mortgage banker, and consistency with working on improving your credit. For more home buying tips, visit the Atlantic Bay blog.