In the world of foreclosures, there’s a term you might come across: “deed in lieu.” But what does it mean, and how does it affect your credit? Let’s break it down in simple terms.

What is a Deed in Lieu?

A deed in lieu of foreclosure happens when you give your house back to the lender to avoid foreclosure. It’s like saying, “Here’s the house, you don’t have to go through the trouble of taking it from me.”

How Does it Affect Your Credit?

When it comes to your credit, a deed in lieu isn’t as bad as a foreclosure, but it still has an impact:

Credit Report: Just like with a foreclosure, a deed in lieu will show up on your credit report. It tells lenders that you didn’t keep up with your mortgage payments and had to give back the house.

Credit Score: While it may not hurt your credit score as much as a foreclosure, it still takes a hit. How much of a hit depends on your overall credit history and other factors.

Future Loans: Having a deed in lieu on your credit report can make it harder to get loans in the future. Lenders might see you as a risk because you didn’t fulfill your mortgage obligations.

Recovery Time: The impact of a deed in lieu on your credit can last for several years. It takes time and good financial behavior to rebuild your credit after such an event.

Conclusion:

In summary, a deed in lieu can have a negative impact on your credit, although not as severe as a foreclosure. It’s important to understand the consequences before considering this option. If you’re facing financial difficulties, it’s best to explore all your options and consult with a financial advisor or real estate professional.

Florida is known as a lien theory state where the property acts as security for the underlying loan. The document that places the lien on the property is called a mortgage.top

How are Florida mortgages foreclosed?

In Florida, the lenders go to court in what is known as a judicial foreclosure proceeding where the court must issue a final judgment of foreclosure. The property is then sold as part of a publicly noticed sale. The court with jurisdiction over a foreclosure is known as the Circuit Court. A complaint is filed in Circuit Court along with what is known a lis pendens. A lis pendens is a recorded document that provides public notice that the property is being foreclosed upon.top

What are the legal instruments that establish a Florida mortgage?

The documents are known as the mortgage, note, and in a commercial transaction, a security agreement. Sometimes the mortgage document is combined with the security agreement. A mortgage is filed to evidence the underlying debt and terms of repayment, which is set forth in the note.top

How long does it take to foreclose a property in Florida?

Depending on the court schedule, it usually takes approximately 180-200 days to effectuate an uncontested foreclosure. This process may be delayed if the borrower contests the action, seeks delays and adjournments of hearings, or files for bankruptcy.top

Is there a right of redemption in Florida?

Florida has a statutory right of redemption, which allows a party whose property has been foreclosed to reclaim that property by making payment in full of the sum of the unpaid loan plus costs. There is a time limit to undertake such redemption.top

Are deficiency judgments permitted in Florida?

Yes, a deficiency judgment may be obtained when a property in foreclosure is sold at a public sale for less than the loan amount that the underlying mortgage secures. This means that the borrower still owes the lender for the difference between what the property sold for at auction and the amount of the original loan.top

What statutes govern Florida foreclosures?

The laws that govern Florida foreclosures are found in F.S. 702.01 et. seq.

Short sales and foreclosures can hurt your credit—here’s how

Credit scores can predict how likely you are to make timely payments, pay off loans, and help a lender understand how “risky” you are as a borrower. Your credit score is based on your lending history and your ability to manage and repay debts as agreed.

Financial slip-ups impact your score, such as failing to make timely payments or letting your mortgage payment slide. If you suffer a short sale or foreclosure, your credit score will suffer too—you’re a potential increased risk for a lender.

If you’re considering a short sale or foreclosure for your home, here’s how much your credit score could drop, how long a foreclosure or short sale will stay on your credit report, and what you can do to reduce the damage.

What Is a Short Sale?

A short sale allows you to sell your home and use the sale proceeds to pay off your mortgage—even if those proceeds don’t amount to the full loan balance. Because lenders often take a financial loss on short sales, this isn’t an option in every situation. You’ll need to reach out to your mortgage lender or servicer directly to inquire if a short sale is possible and any associated requirements.

“Most banks would prefer that a homeowner who has fallen behind on their payments or can no longer afford their home move forward with a short sale,” Yawar Charlie, a Los Angeles-based real estate agent, told The Balance via email. “It is more cost-effective for the lender, and faster.”

A “deficiency” after is the difference between your mortgage and your property’s value. You may be responsible for the deficiency (depending on your state), or your lender may waive this amount, freeing you from responsibility for the difference.

What Is a Foreclosure?

If you fail to make your mortgage payments, you may face foreclosure when the lender seizes your property and sells it to make up for their financial losses. It typically takes four missed payments (after 120 days) to kick off foreclosure proceedings.1

The exact foreclosure process varies by state, but you should receive notice in the mail if a foreclosure is headed your way.

Open and read all letters from your lender or servicer, and consider federal government assistance in avoiding foreclosure.

How a Short Sale Affects a Credit Score

According to Tony Wahl, director of operations at online credit analysis platform Credit Sesame, short sales (as well as foreclosures) should be considered “a last resort.”

“The short sale process is complicated, lengthy, and will have negative ramifications for a homeowner’s credit and finances,” Wahl said in an email to The Balance.

How much can a short sale impact credit, though? Data from the Fair Isaac Corporation (FICO) shows short sales can reduce a consumer’s credit score anywhere from 50 to 160 points, depending on where their credit started. For short sales, the impact is more significant when there’s a deficiency balance.2

The impact is more noticeable for consumers with good credit—meaning a high score or few debts and overdue payments—than someone with an already low score. For example, someone with a higher score could see their credit score drop up to 20% in the worst-case scenarios, while a short-seller with a lower score might only see a 15% drop in the same situation.2

A short sale could stay on your credit history for anywhere between three to seven years.2 However, consumers with a short sale on their record may be able to buy again in just two years in certain circumstances.3

“When it comes time for that consumer to buy a new home, most mortgage lenders will be more lenient with a prior short sale than with a prior foreclosure,” Wahl said.

If you think you’ll buy another home sometime in the future, be sure to get a letter from your lender confirming the short sale, which could help you qualify for a new loan.

How a Foreclosure Affects a Credit Score

Foreclosures have a slightly worse impact on credit score, according to FICO. Depending on their starting score, most homeowners who suffer a foreclosure see their credit scores drop between 85 and 160 points, or about 12% to 20%.2

For example, someone with a “good” starting score of 680 could decrease to between 575 and 595, which is in the “poor” to “fair” score ranges. Someone with a “very good” score of 780 may decrease to between 620 and 640, or the “fair” score range.

A foreclosure can impact a consumer’s credit for up to seven years. Of the 7 million-plus Americans who experienced foreclosure between 2004 and 2015, a little over half still had a credit score rating falling into the “poor” range at the end of 2015.4

Mortgage loan qualification is difficult with a foreclosure on your record, and can mean waiting as much as seven years to buy a new home. A foreclosure won’t be removed from your credit history until seven years after the first missed payment.

Late Payments and Your Credit Score

Late payments have one of the most significant negative impacts on credit score. Late mortgage payments could lead to a double-whammy on your credit score, impacting it long before your short sale or foreclosure happens.

“In both circumstances, the lender will be reporting your late or missed payments,” Charlie said. “Therefore, your credit score will already be negatively impacted—and most late payments take several years to fall off your credit report.”

According to FICO, falling just 30 days behind on your mortgage can result in a credit score drop of up to 110 points. At 90 days, the decrease could go up to 130 points.2

Rebuild Your Credit After a Short Sale or Foreclosure

A short sale or foreclosure doesn’t cause permanent credit damage. Though it takes time, there are ways to improve your score and your future financial options.

According to Wahl, you should aim to make consistent monthly payments on any other debts.

“Remind yourself that this is a long game and will take time,” he said.

In the meantime, you can request help from the National Foundation for Credit Counseling or another nonprofit credit counseling agency. Counselors can walk you through your options for improving your credit and help you toward recovery from your short sale or foreclosure.

Get an overview of basic foreclosure terms, steps in a foreclosure, and possible defenses to foreclosure.

If you fall far enough behind in your mortgage payments, you’ll likely lose your home to foreclosure. Foreclosure is the legal process that allows a lender, or the subsequent loan owner, to sell your property to satisfy the debt you owe. (To learn what to do—and what not do—if you’re facing a foreclosure, see Foreclosure Do’s and Don’ts).

Read on to get an overview of the parties and terminology involved in a home loan transaction, find out the general steps in the foreclosure process, and learn about some defenses that might be available to you in a foreclosure.

Home Loan Transactions: Parties Involved

The key parties involved in most home loan transactions and foreclosures are:

The borrower. The borrower is the individual (the homeowner) who borrows money and pledges the home as security to the lender for the loan. The borrower is sometimes called the “mortgagor.”

The lender. The lender originates the loan. Sometimes the lender is called the “mortgagee.”

The investor. An investor buys loans from lenders. (Fannie Mae and Freddie Mac are considered investors.)

The servicer. The servicer—the company you make your monthly payment to—handles the loan account. Often the servicer is a third party that manages the account on behalf of the lender or an investor for a fee. A servicer’s duties include collecting and processing loan payments, as well as initiating and monitoring a foreclosure when a borrower stops making payments.

Home Loan Transactions: Terminology

Buying a home normally involves a large amount of money so it’s common for a buyer to take out a loan, rather than pay the entire amount in cash. As part of a home loan transaction, a borrower typically signs two main documents: a promissory note and a mortgage (or deed of trust).

A promissory note is like an IOU. A promissory note is the document that contains a borrower’s promise to repay the amount borrowed.

Mortgages and deeds of trust give the power to foreclose. A mortgage—or, in some states, a deed of trust—is the contract that gives the lender the right to foreclose if the borrower doesn’t make payments on the loan. . When the lender records this document in the land records, it creates a lien on the home.

Endorsements and assignments. Promissory notes are transferable, and banks often buy and sell home loans. When a loan changes hands, the promissory note is endorsed (signed over) to the new owner of the loan. The seller documents the transfer by recording an assignment of the mortgage or deed of trust in the land records.

Foreclosure Steps

If you default on your loan by falling behind in payments or breaching the agreement in some other way, the servicer will probably refer the loan an attorney or trustee for foreclosure. Foreclosure works differently in each state, but there are two basic types: judicial foreclosures and nonjudicial foreclosures.

Judicial foreclosures. In a judicial foreclosure, an attorney files a lawsuit on behalf of the lender or investor in court to foreclose the home. You’ll receive a copy of the complaint, sometimes called a petition, which starts the foreclosure. You then get a certain number of days, like 30, to respond to the lawsuit. If you don’t file an answer in court—or if you file a response, but the court decides the foreclosure should go ahead—the court will grant a judgment of foreclosure in favor of the foreclosing party and set a sale date. The foreclosure sale is typically an auction where the public, as well as the foreclosing party, may bid on the property. The highest bidder becomes the new owner of the home.

Nonjudicial foreclosures. All states allow judicial foreclosures, but about half also permit nonjudicial (“power of sale”) foreclosures. In a nonjudicial foreclosure, an attorney or trustee (again, on behalf of the lender or investor) completes certain out-of-court steps. Typically, a nonjudicial foreclosure involves one or more of the following steps, depending on state law:

mailing the borrower a notice of default that tells how much time the borrower has to reinstate (get caught up on payments)

recording the notice of default in the local land records office, and

mailing the borrower a notice of sale that states when the property will be sold. Like in a judicial foreclosure, the property is usually sold at a public auction.

Depending on state laws, a borrower might get a combined notice of default and sale, a notice of sale, or notice by publication in a newspaper and posting on the property or in a public place.

After Foreclosure: Right to Redeem, Deficiency Judgments

You own your home up until the foreclosure sale. This means you may legally stay there until this time. In addition, depending on state law, you might be able to stay in the home until the redemption period expires or until some other action, such as ratification of the sale, occurs.

What is a redemption period? Certain states have laws giving a foreclosed homeowner the right to regain ownership of the home—called “redeeming” the property—after a foreclosure sale by reimbursing the buyer for the amount paid at the sale or by repaying the full amount of the mortgage debt.

What is a deficiency judgment? Sometimes, a foreclosure sale doesn’t bring in enough money to fully repay the home loan. When this happens, the difference between the sale price and the amount owed is called a deficiency. In certain states, the foreclosing party can get a personal judgment—a deficiency judgment—against the borrower for this amount.

Sometimes, A Reforeclosure Is Necessary to Clear Up Title to the Property

Homeowners occasionally face back-to-back foreclosures when the title to the property has problems after the first foreclosure. The second foreclosure is called a “reforeclosure.”

Defenses to Foreclosure

Depending on state law and your individual circumstances, you might have a defense to a foreclosure. A few potential foreclosure defenses include:

you’re entitled to protection from foreclosure under the Servicemembers Civil Relief Act

the servicer didn’t follow state foreclosure procedures

the servicer didn’t follow federal mortgage servicing laws, or

the servicer made a serious mistake.

Talk to a Lawyer

While this article provides a general picture of how foreclosure works, laws vary from state to state. To get specific information about your state’s foreclosure procedures and how they apply to your particular situation, consider talking to a local foreclosure attorney.

If you’re struggling to pay the property taxes on your home, you could be at risk of losing the property to foreclosure or a tax sale.

If you’re struggling to pay the property taxes on your home, you could be at risk of losing the property to foreclosure or a tax sale. But you might be able to either reduce the amount of property tax that you have to pay or buy yourself some extra time to get caught up on what you owe.

Challenging Your Home’s Assessed Valuation

One thing you can do to reduce the property taxes you have to pay is to challenge the assessed value of your home. The property taxes are primarily based on your home’s assessed value.

All states have specific procedures for challenging—or “appealing”—the assessed value of the home. Typically, you’ll need to dispute the value shortly after you receive the bill. To prevail in your challenge, you must show that the estimated market value placed on your property is either inaccurate or unfair. Also, some states require that you pay the bill before making the appeal. You’ll then typically get a refund if you’re successful in your challenge.

Be sure to follow the procedures carefully otherwise you might lose the appeal. Check the tax assessor’s website online or review your property tax bill to learn about the specific procedures, as well as what sort of documents and evidence you’ll need, to make your challenge to the value the assessor placed on your home.

Abatement, Deferral, and Repayment Programs

Each state has property tax abatement (reduction) or exemption programs that allow certain homeowners to reduce the amount of property tax they must pay based on age, disability, income, or personal status. For example, older homeowners and veterans often are entitled to a reduction of their property taxes. Ordinarily, you’ll have to apply for the abatement and provide proof of eligibility.

In some states, abatement isn’t possible if you’re already delinquent in your tax payments. But you might qualify for:

a deferral (where you’re allowed to postpone paying the taxes if you meet eligibility requirements), or

a repayment plan.

In addition, many states permit the taxing authority to compromise on the amount of taxes that are due or to waive penalties and interest.

Losing Your Home for Failure to Pay Property Taxes

When you don’t pay your property taxes, the taxing authority could sell your home—or its lien on the property—to satisfy your debt. (To get details on how both of these processes work, see What Happens If You Don’t Pay Property Taxes on Your Home?

Or, your mortgage lender might pay the taxes itself and then bill you. If you fail to reimburse the mortgage lender, it might foreclose on your home. If you’re facing a potential foreclosure, consider contacting an attorney to find out about your options.

If you decide not to fight the foreclosure of your home, you don’t have to leave right away. Learn more.

If you don’t fight your foreclosure or take any steps to work out an alternative, the foreclosure will move forward on a schedule dictated by your lender’s and loan servicer’s workload and policies, and federal and state law.

You Don’t Have to Leave Right Away

The single most important point to understand is that you don’t have to leave your house just because you’re behind in payments or because foreclosure proceedings have started. In most states, you’ll probably be able to stay long enough to plan for the future by saving all or some of the money that you’re no longer putting toward the mortgage.

Example. Joshua and Ellen got in over their heads and now can’t afford the $3,000 monthly payment on their mortgage. They decide to let the house go. They already know that federal mortgage servicing law requires the servicer to wait at least 120 days after they quit making payments before officially starting the foreclosure. They then consult with a local foreclosure attorney to see how much more time they have. They learn that:

In their state, they’ll get notice about the foreclosure sale four weeks before it happens in what’s called a notice of sale.

They can file for Chapter 7 bankruptcy and delay the sale by three additional months. Bankruptcy will also let them leave without owing the lender anything. They otherwise could face a deficiency judgment in their situation.

Under their state’s laws, they’ll get to stay in the house during the redemption period after the foreclosure sale.

Altogether, they will have about a year of living in the house without making payments, and if they can save at least $2,000 a month, they will have roughly $24,000 in the bank when they set out to seek new shelter.

How Long You’ll Get to Stay In the Home

How much time you’ll get to remain in your house depends on many factors, including:

whether the foreclosure is judicial or nonjudicial (judicial foreclosures usually take longer than nonjudicial ones)

whether you get the right to participate in foreclosure mediation, which might prolong the process

whether you get the right to live in the home during a post-sale redemption period, if there is one, after the foreclosure sale, and

whether part of your strategy involves filing for bankruptcy before the foreclosure sale, which provides an additional two to three months’ delay.

Getting Help

To find out approximately how long you can remain in your home in a foreclosure in your state and in your situation, consider talking to a foreclosure attorney or a HUD-approved housing counselor.

Your credit score will take a hit after foreclosure, short sale, or deed in lieu of foreclosure. Learn more.

If you stop making payments on your mortgage loan, you’ll probably go through a foreclosure, which will damage your credit score. Even if you manage to avoid going through a foreclosure with a short sale or a deed in lieu of foreclosure, your credit score will take a major hit.

Read on to learn the basics about why credit scores matter, how they work, and how a foreclosure, short sale, or deed in lieu of foreclosure typically hurts your credit score.

Credit Scores: Why They Matter, How They Work

If you apply for home loan or other form of credit, like a credit card or a car loan, the creditor will take a look at your credit score from one or more of three major credit reporting agencies—Equifax, Experian, and TransUnion—as part of the process of figuring out whether or not to extend you the credit. Credit scores, in theory, indicate whether you’re likely to default on the loan. Generally, people with lower credit scores are more likely to default on payments than people with higher scores.

Your credit score is based on what’s in your credit report, including:

the payment history on your outstanding debts

how many debts you have and how much you owe

how long your credit history is

the different kinds of credit you have

whether you’ve recently applied for new credit, and

whether you’ve been through a foreclosure or have declared bankruptcy.

Credit scoring companies use “models” that analyze this data and then assign a credit score based on that information. Different companies use different scoring models so a person’s credit score usually varies by a few or many points depending on which company and model generated the score.

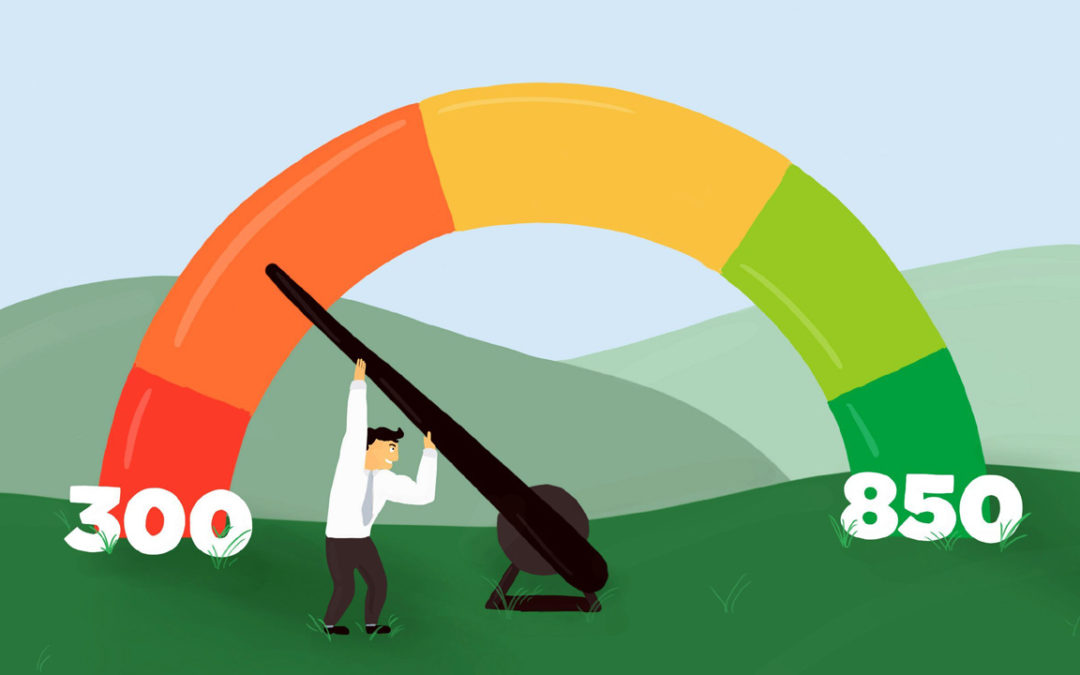

Typically, credit scores—like scores from the largest and most universal credit scoring company called FICO—range from 300 to 850. VantageScore, which is another credit scoring company, also uses a range of 300 to 850 in its newer model, while its older models have a range of 501 to 990.

How Foreclosure Affects Your Credit Score

Both missed mortgage payments and a foreclosure itself will damage your credit score.

How missed (or late) payments affect your score. Under federal mortgage servicing rules, in most cases, a borrower has to be more than 120 days delinquent on payments before the servicer can officially start a foreclosure. The lender reports the missed payments as 30 days late, 60 days late, 90 days late, and the like to the credit reporting agencies. According to FICO, a person’s credit score drops about 50 to 100 points when the lender reports the account as 30 days past due and each subsequent delinquency lowers the score further.

How foreclosure affects your score. After a foreclosure, your score will likely go down by at least 100 points. How much the score actually falls depends to some extend on your score before the foreclosure started. Someone with a higher score prior to a foreclosure generally loses more points than someone who already has a low score. According to FICO, a person who has a credit score of 680 prior to a foreclosure loses 85 to 105 points following a foreclosure. But a person who has a credit score of 780 prior to a foreclosure loses 140 to 160 points.

How a Short Sale or Deed in Lieu of Foreclosure Affects Your Credit Score

Completing an alternative to foreclosure, like a short sale or deed in lieu of foreclosure (DIL), will also usually hurt your credit score.

Generally, short sales and DILs have a similar effect on a person’s credit score. Much like with a foreclosure, if you have high credit score before the short sale or DIL—say you complete one of these transactions before missing a mortgage payment—the transaction will cause more damage to your credit score. Though, if you’re behind on your payments and already have a low score, a short sale or DIL won’t cause you to lose as many points as someone who has a high score.

Also, if you’re able to avoid owing a deficiency after the short sale or deed in lieu of foreclosure, your credit score might not fall quite as much.

Beware of Credit Repair Scams

Scammer credit repair companies sometimes try to sell their services claiming that they can easily repair your credit score or even clear a foreclosure off your credit report. However, foreclosures and many other negative items typically stay on a credit report for seven years and you can’t magically eliminate them—though the impact of these events on your score will lessen over time. Also, paying your other debts on time and disputing incomplete and inaccurate information in your credit report can improve your score.

Getting Help

If you want more information about how to improve your credit score, consider talking to a credit repair attorney. If you have questions about ways to avoid a foreclosure, consider talking to a foreclosure attorney or a HUD-approved housing counselor.

If you’re facing a foreclosure, be on the lookout for foreclosure rescue companies—specifically, mortgage modification companies—that falsely claim they can help you save your home.

If you’re a homeowner struggling to make your mortgage payments and facing a possible foreclosure, a scammer might try to contact you. Scammer people and companies say that they help homeowners save their home—usually through a mortgage modification—but often leave homeowners in worse shape than before.

Mortgage Modification Scams

Borrowers who’re struggling to make their mortgage payments might have a number of options to get caught up on the payments, including a modification, forbearance agreement, or repayment plan. You can apply for any of these options, including a modification, on your own without paying for assistance. But scammers might send you mailings trying to convince you that you’re better off hiring their company to help you with the process. (To learn what to do—and what not do—in the modification process, read Do’s and Don’ts for Getting a Loan Modification.)

Solicitations and mailings that you get from a modification company tend to look official, even though they aren’t. The name of the company might sound like the government has endorsed the program or the mailing might refer to official U.S. government programs. Typically, scammer mailings claim you can “Stop foreclosure now!” or “Over 90% of our customers get a loan modification.” These statements are ploys to get you to call the company. Once you do, the main goal of a scammer modification company is to separate you from your money by getting you to pay for the company to—supposedly—help you get a modification.

Forensic Loan Audits and Securitization Audits

A modification company might try to convince you to pay for a “forensic loan audit” or a “securitization audit” to improve your chances of getting a mortgage modification.

What’s a Forensic Loan Audit?

In a forensic loan audit, in theory, a loan auditor reviews paperwork from when you took out your mortgage to see if the lender complied with the law. If the audit reveals legal violations, you can supposedly then use the results to strong-arm the lender into giving you a modification. But the way most companies conduct the audit is that a processor enters your information into a compliance software program, and the program prepares a very basic report. In most cases, no errors or only minor errors are found. The sales person might say that the results of such an audit will force the servicer into giving you a modification, but this is rarely true.

What’s a Securitization Audit?

In a process called securitization, multiple loans with similar characteristics are pooled and then sold in the secondary market, often to a trust. A securitization audit will supposedly reveal whether your loan was securitized and, if so, whether the securitization was done correctly. But securitization audit reports usually just give you publicly available information and make unsupported conclusions of law that aren’t useful when trying to get your loan modified.

Modification Companies: High Fees for Little or No Services

Most foreclosure scammers, including modification companies, exploit a homeowner’s trust and desperate situation by:

charging very high fees for services the homeowner could easily do without assistance, like sending in documentation to the servicer

charging money for certain services and then not doing anything to earn the fees, or

taking steps that actually hurt the homeowner, like missing deadlines or allowing a foreclosure sale to happen.

There’s nothing that a modification company can do that you can’t do yourself. In fact, the company might even hurt your chances of getting a modification, like if it:

neglects to send in your paperwork to the servicer (the company you make your payments to, which also handles modification applications)

sends the wrong documents to the servicer, or

fails to return the servicer’s phone calls.

By the time you realize the company is just running a scam, there might not be enough time to reinstate the loan, work out an alternative to foreclosure, sell the home, or find effective assistance. In almost all cases, you’re better off applying for a modification directly with the servicer yourself or—if you find the servicer is unhelpful or is dual tracking your application—hiring a reputable attorney to help you.

Some States Have Laws to Prevent Foreclosure Rescue Scams

To protect homeowners in financial difficulty from losing their homes to foreclosure rescue scams, the Florida legislature enacted the Foreclosure Rescue Fraud Prevention Act. This law imposes tight restrictions on anyone offering services purporting to help you save your residential property from foreclosure. New Jersey also has a law designed to prevent foreclosure consultants from taking advantage of distressed homeowners.

Tips to Help You Avoid Becoming the Victim of a Modification Scam

Here’s how you can make sure that you don’t become a victim of a modification scam.

Don’t pay upfront fees. If a modification company demands a large upfront fee from you, beware. Many states have laws prohibiting modification companies from collecting money before performing services, as well as other restrictions on foreclosure rescue activities.

Don’t pay a modification company rather than your servicer. Sometimes, modification companies advise people to pay the company’s fee instead of making their mortgage payments. This is a red flag. The company might take your money, fail to get you a modification (or not even try), and then you’ll be even further behind on your payments.

Don’t ignore your servicer or lender. Modification companies often tell people to stop communicating with their servicer and let the company do all negotiating. But that’s not a good idea. You should continue to talk (and listen) to your loan servicer. There’s no magic trick or secret skills involved in “negotiating” a modification. You submit an application and the servicer will let you know if you qualify. Plus, if you keep the lines of communication open, you might learn about a workout option you hadn’t previously considered.

Do work with a HUD-approved housing counselor. If you need help working out a modification, you can get free help from a HUD-approved housing counseling agency.

Reporting Scams

If you suspect you’re a victim of a modification scam, contact:

Loan modifications, forbearance agreements, and repayment plans are different ways that borrowers can avoid foreclosure. Read on to learn the difference between these options and how they can help you if you’re having trouble making your mortgage payments.

Loan Modifications

A loan modification is a permanent restructuring of the mortgage where one or more of the terms of a borrower’s loan are changed to provide a more affordable payment. With a loan modification, the loan owner (“lender”) might agree to do one of more of the following to reduce your monthly payment:

reduce the interest rate

convert from a variable interest rate to a fixed interest rate, or

extend of the length of the term of the loan.

Generally, to be eligible for a loan modification, you must:

show that you can’t make your current mortgage payment due to a financial hardship

complete a trial period to demonstrate you can afford the new monthly amount, and

provide all required documentation to the lender for evaluation.

Required documentation will likely include:

a financial statement

proof of income

most recent tax returns

bank statements, and

a hardship statement.

Many different loan modification programs are available, including proprietary (in-house) loan modifications, as well as the Fannie Mae and Freddie Mac Flex Modification program.

If you’re currently unable to afford your mortgage payment, and won’t be able to in the near future, a loan modification might be the ideal option to help you avoid foreclosure. (Read about how to get a loan modification. Also, be sure to learn the do’s and don’ts when trying to get a modification.)

Forbearance Agreements

While a loan modification agreement is a permanent solution to unaffordable monthly payments, a forbearance agreement provides short-term relief for borrowers.

With a forbearance agreement, the lender agrees to reduce or suspend mortgage payments for a certain period of time and not to initiate a foreclosure during the forbearance period. In exchange, the borrower must resume the full payment at the end of the forbearance period, plus pay an additional amount to get current on the missed payments, including principal, interest, taxes, and insurance. The specific terms of a forbearance agreement will vary from lender to lender.

If a temporary hardship causes you to fall behind in your mortgage payments, a forbearance agreement might allow you to avoid foreclosure until your situation gets better. In some cases, the lender might be able to extend the forbearance period if your hardship is not resolved by the end of the forbearance period to accommodate your situation.

In forbearance agreement, unlike a repayment plan, the lender agrees in advance for you to miss or reduce your payments for a set period of time.

Repayment Plans

If you’ve missed some of your mortgage payments due to a temporary hardship, a repayment plan may provide a way to catch up once your finances are back in order. A repayment plan is an agreement to spread the past due amount over a specific period of time.

Here’s how a repayment plan works:

The lender spreads your overdue amount over a certain number of months.

During the repayment period, a portion of the overdue amount is added to each of your regular mortgage payments.

At the end of the repayment period, you’ll be current on your mortgage payments and resume paying your normal monthly payment amount.

This option lets you pay off the delinquency over a period of time. The length of a repayment plan will vary depending on the amount past due and on how much you can afford to pay each month, among other things. A three- to six-month repayment period is typical.